Technology

Semiconductors: Huawei’s Tau Scaling Law reframes packaging-led scaling as China’s post-sanctions roadmap

Read more

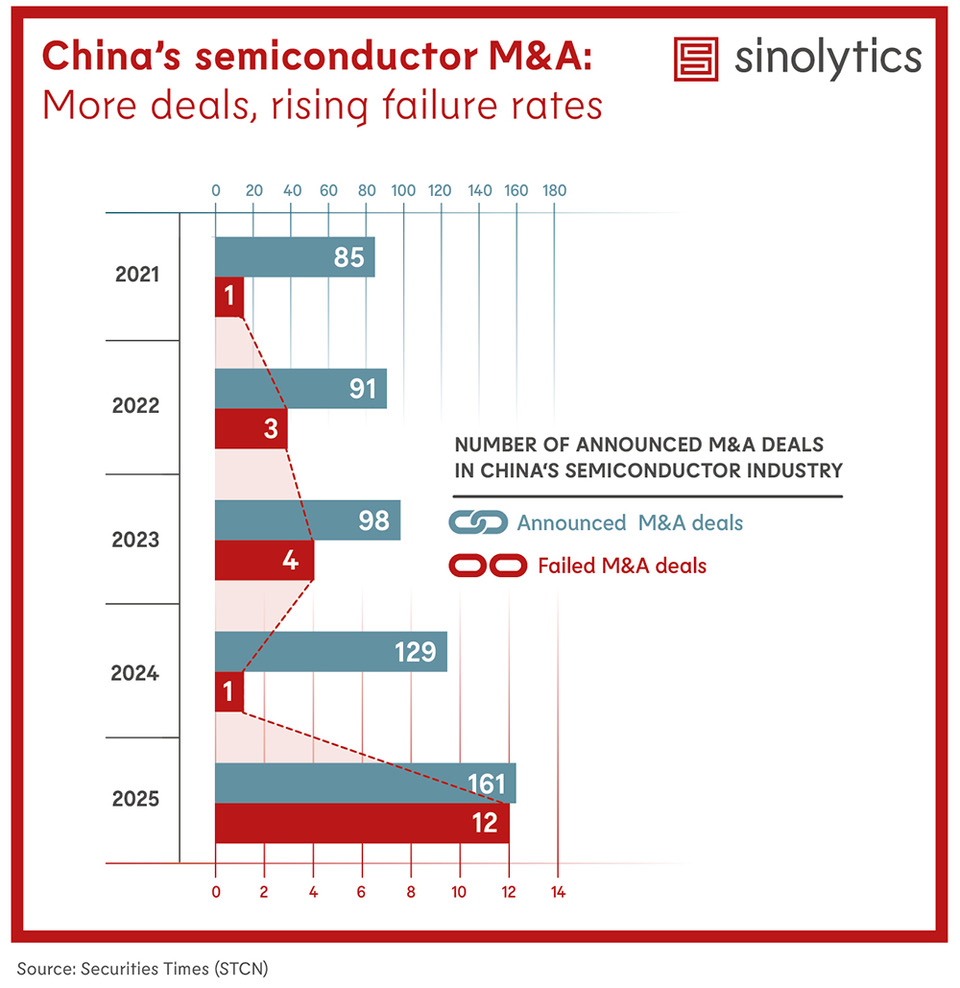

China’s semiconductor sector is entering a phase of accelerated consolidation, driven by both market pressures and state‑backed industrial policy. Two patterns stand out.

First, horizontal and vertical integration is intensifying. IC design firms are merging to broaden portfolios, while equipment manufacturers increasingly acquire upstream and downstream suppliers to strengthen technological coherence. Notable recent moves include NAURA Technology’s stake in photolithography supplier Kingsemi and Hwatsing’s takeover of Xinyu Semiconductor to unify its CMP equipment and service capabilities.

Second, consolidation is particularly pronounced in IC design and semiconductor equipment. Of 38 significant transactions reviewed by Sinolytics, 50% were initiated by design firms and 34% by equipment and materials companies, underscoring where competitive pressure is strongest.

Government-backed efforts to reduce the large number of small and mid‑sized equipment manufacturers into fewer, platform‑scale champions further reinforce this trend. The rising domestic equipment adoption rate – from 25% in 2024 to 35% in 2025 – suggests these efforts are beginning to reshape supply chain outcomes.

However, consolidation momentum remains fragile. 2025 also saw a record number of failed deals. These high‑profile failures reflect structural issues: elevated semiconductor valuations, ample access to government subsidies, and the relative ease of IPO financing continue to reduce companies’ incentives to merge. Without addressing these systemic distortions, China’s pathway toward deeper consolidation will remain uneven.

China’s push toward semiconductor consolidation affects any company sourcing from or competing with Chinese suppliers. A more concentrated landscape could change supplier dynamics, while continued deal failures signal ongoing instability that companies must factor into risk planning.

Sinolytics helps companies interpret China’s consolidation trends, understand the drivers behind successful and failed deals, and identify what this means for supply chains, competition, and long‑term strategic planning.

We do so through targeted market analysis, supply‑chain mapping, competitive intelligence, and scenario modelling, always grounded in verified data and China‑specific policy understanding.

Our team can walk you through what this consolidation dynamic means for your sector, your suppliers, and your China strategy, without over‑interpretation and focused strictly on evidence‑based insights.