Technology

China's automotive chip race: From dependency to domestic innovation

Read more

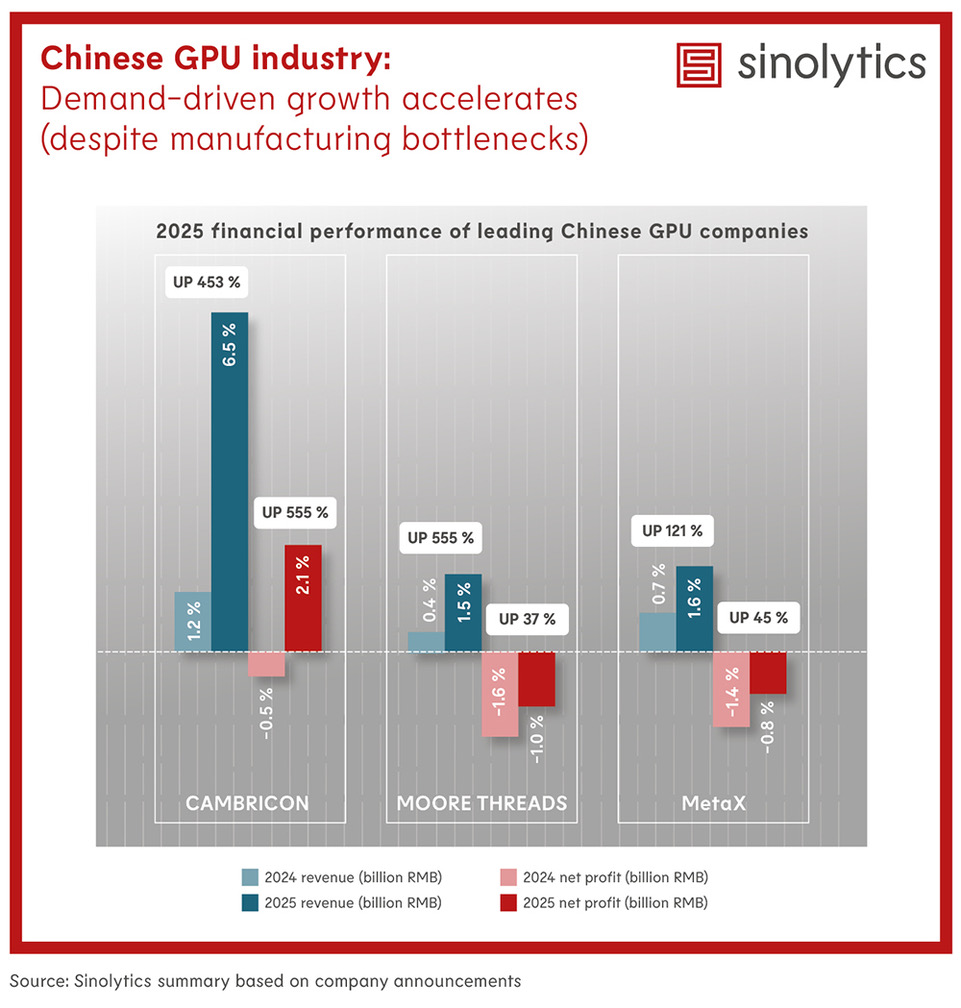

In 2025, leading listed Chinese GPU companies, including Cambricon, Moore Threads, and MetaX, reported more than double year‑on‑year revenue growth, alongside significantly narrowed losses. MetaX attributed its improvement to the emergence of large‑scale repeat purchases from downstream customers, while Moore Threads noted that continued heavy R&D investment remains a key constraint on near‑term profitability.

Cambricon achieved profitability in 2025, becoming one of the few domestic GPU vendors to successfully demonstrate a scalable and profitable business model. The company attributes th turnaround not to cuts to R&D spending, but to rapid product volume growth fueled by surging AI compute demand.

The exponential growth in large‑model inference workloads is boosting demand for GPUs. Recent data show that Chinese models reached 5.16 trillion weekly tokens on OpenRouter, compared with 2.7 trillion for U.S. models, led by MiniMax, Kimi, GLM‑5, and DeepSeek. At home, average daily token usage by Chinese companies rose from 10.2 trillion in 2025H1 to 37.0 trillion in 2025H2, with Qwen taking the lead. This explosion in inference demand is shifting domestic GPUs from policy‑driven substitution toward demand‑driven adoption.

Despite steady progress in single‑card performance and selected use cases, Chinese GPUs still lag NVIDIA substantially in software ecosystems and system‑level delivery capabilities. NVIDIA’s financial disclosures highlight the scale of this gap: NVIDIA’s revenue alone is tens of times larger than the combined revenue of all Chinese GPU vendors.

Access to advanced manufacturing capacity remains a bottleneck for Chinese GPU makers. Allocation of advanced capacity is reportedly centrally coordinated, with Huawei receiving top priority, followed by companies such as Cambricon, Alibaba T‑Head, Sugon, Moore Threads, and MetaX, underscoring persistent supply‑side constraints despite strong demand.

Image created with ChatGPT.