Technology

No more middle ground: What the Meta-Manus case means for tech companies

Read more

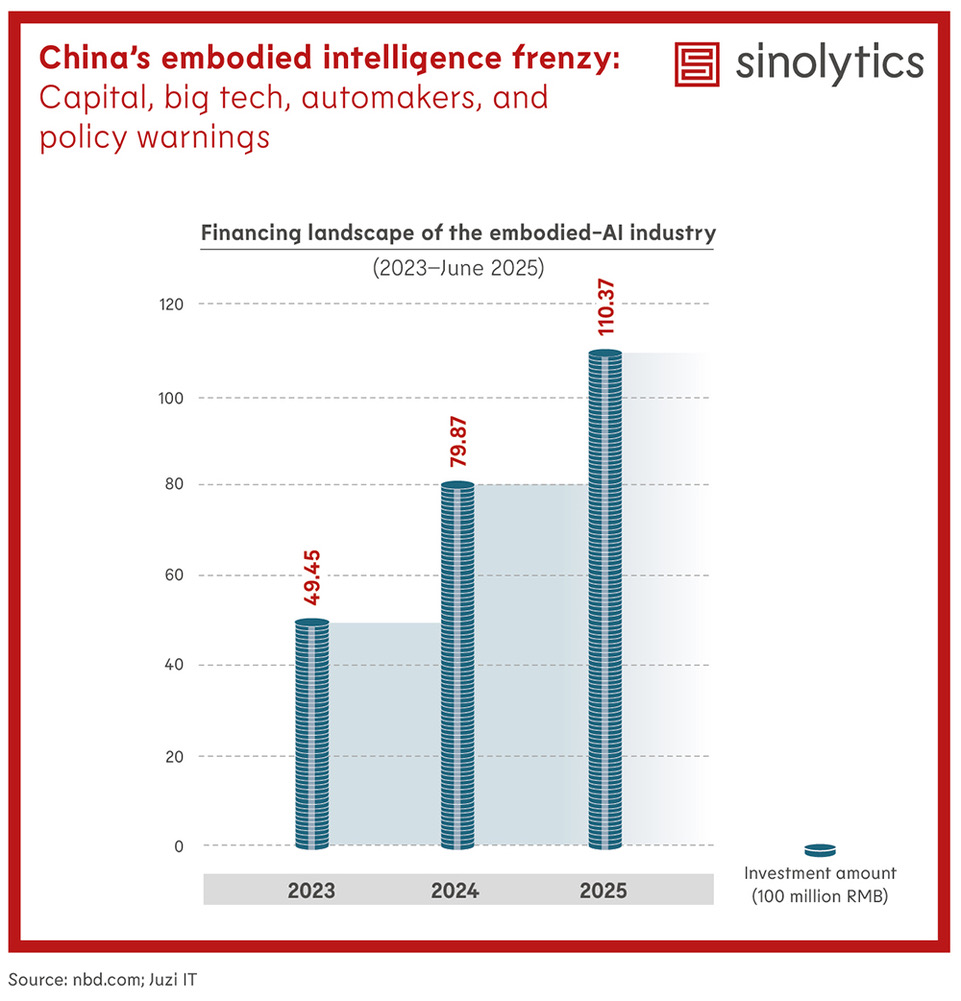

The embodied intelligence track has become one of China's most active investment arenas. Since early 2023, nearly 200 financing events have been recorded, with cumulative funding surpassing 230 billion RMB. In 2025 alone, 35 deals were disclosed in November, almost half exceeding 100 million RMB, underscoring investor confidence in humanoid robotics as the next industrial frontier.

Alibaba, Meituan, and Tencent are aggressively securing their “entry tickets” to embodied intelligence. Tencent has invested in UBTECH and Agi Bot, while Meituan has taken stakes in Galaxy General Robotics and Unitree Robotics. Alibaba, focusing on AI ecosystems, backs firms like Robot Era and offers its Qianwen large language model to robotics developers. This strategic positioning reflects a broader race to dominate AI-driven hardware platforms.

China's automotive giants are leveraging supply chain synergies to enter humanoid robotics. Changan, Dongfeng, and XPeng have unveiled prototypes and committed to mass production by 2028–2030. Their logic is clear: robotics and smart vehicles share core technologies, perception, decision-making, and precision control, making cross-industry integration a natural next step.

While embodied intelligence was officially listed in China's 2025 government work report as a "future industry," regulators are now signalling caution. The National Development and Reform Commission recently warned of “duplicate projects” and overheating risks, urging a shift from blind expansion to value-driven growth. This marks a critical inflection point for the sector.