Technology

No more middle ground: What the Meta-Manus case means for tech companies

Read more

The policy design has evolved well beyond its original fuel cell vehicle focus. China is now rolling out a 1+N+X framework: a unified national hydrogen strategy (1) underpinning a set of industrial applications (N) — spanning green fuels, green metallurgy, and chemicals, alongside a growing range of innovative applications (X) including heavy transport beyond FCEVs, long-duration energy storage, and electronics manufacturing. This architecture signals that hydrogen is being repositioned as a versatile decarbonization vector for hard-to-abate sectors, not simply a mobility fuel. The industrial N-layer is particularly significant, as green steel and green chemicals represent far larger hydrogen demand pools than transport.

To accelerate real-world deployment, Beijing has designated five regional city clusters as hydrogen demonstration zones, covering major industrial corridors from Beijing-Tianjin-Hebei to the Pearl River Delta. Each cluster is eligible for up to 1.6 billion RMB in fiscal rewards over four years, disbursed on a performance basis. This incentive structure is designed to drive integrated ecosystem development, connecting electrolyzer deployment, hydrogen production, distribution infrastructure, and end-use applications rather than subsidizing isolated technology demonstrations.

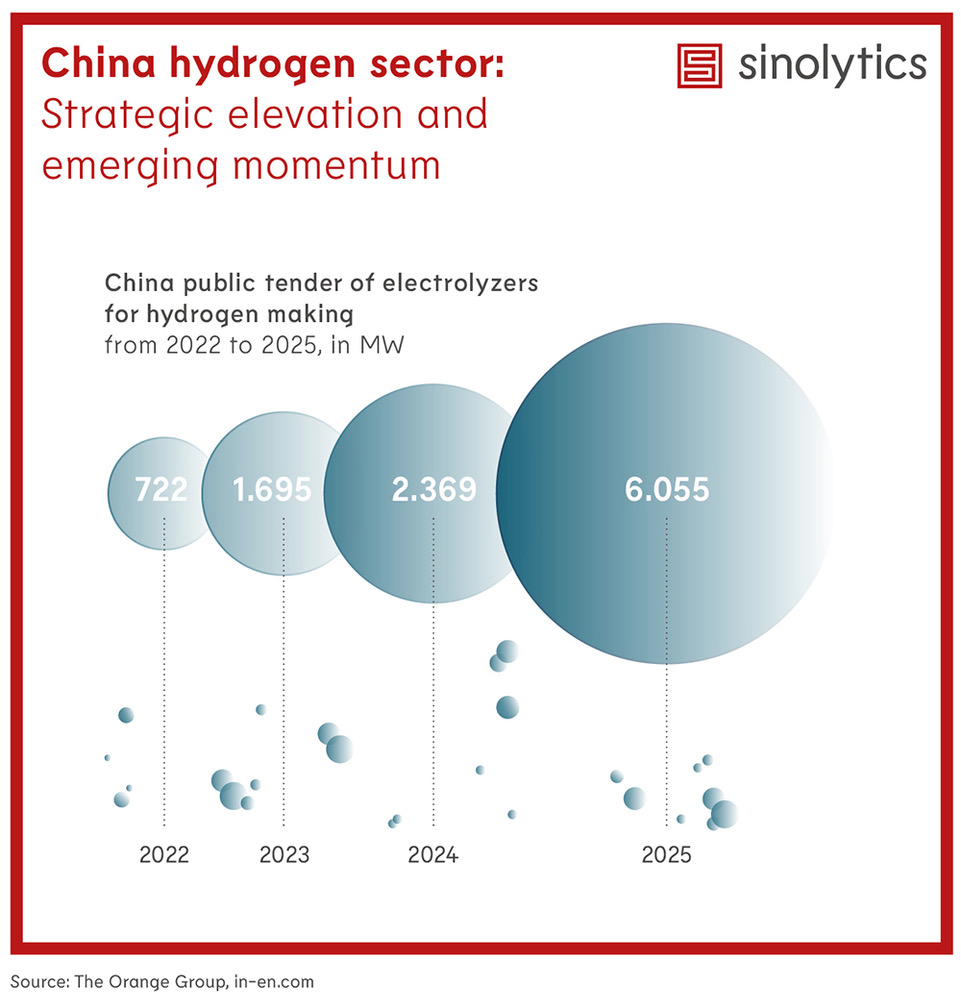

The electrolyzer tender data provides the clearest quantitative signal of execution pace. Public tender volumes for electrolyzers grew from 722 MW in 2022 to 1,695 MW in 2023 and 2,369 MW in 2024, before surging to 6,055 MW in 2025, an approximately eightfold increase over three years and a compound annual growth rate above 100%. Alkaline (ALK) technology continues to dominate tendered capacity at over 90%, reflecting China's deeply integrated domestic supply chain and cost advantage; ALK stacks are available at USD 300–500/kW, much lower than the cost of Western equivalents. PEM's share, while still small, is growing as Chinese manufacturers aggressively close the technology gap with state support. Manufacturing capacity now far exceeds current deployment, creating a significant overhang.

Chinese electrolyzer manufacturers are increasingly targeting international markets, following the same export-led scaling playbook seen in solar PV and EV batteries. Key targets include the Middle East and Africa where large-scale renewable resources make green ammonia and green hydrogen economically attractive, as well as European and North American markets where policy incentives are strongest. Longi Hydrogen has publicly stated it expects international sales to exceed 50% of revenue within three years. PEM stack prices have already fallen 40% between 2022 and 2024 via subsidized scaling. The primary headwind to export growth is local content and supply chain localization requirements in the EU, India, and elsewhere, which are being designed in part to limit Chinese electrolyzer penetration.

Taken together, The Chinese government demonstrates a structural, not cyclical, commitment to hydrogen. China is executing a familiar industrial policy playbook with speed and scale. For global electrolyzer manufacturers and green hydrogen project developers, this raises both a cost benchmark challenge and a supply chain dependency risk that will define the competitive dynamics of the sector through 2030 and beyond.

Header image: AI generated.