Technology

China's OpenClaw push: Districts enter a high-value subsidy race

Read more

DRAM, Dynamic Random‑Access Memory, the short‑term working memory in all digital devices, is in short supply for consumer products such as laptops, smartphones, tablets and TVs. The reason is simple: manufacturers are shifting more of their production capacity toward high‑value memory for AI and data‑center servers. As a result, normal electronics receive a smaller share of available supply.

Because of this imbalance, electronics manufacturers are more willing to qualify additional DRAM suppliers to ensure consistent delivery and reduce pricing risks. This shift opens a practical window for Chinese companies to enter or expand in certain segments of the global DRAM market.

China's opportunity lies mainly in DDR4 and LPDDR4/LPDDR4X, which are DRAM generations widely used in consumer devices. These older types do not require cutting‑edge technology, and buyers are primarily looking for stable supply, acceptable performance, and competitive pricing. Early versions of DDR5 may also offer a limited entry point, as long as they are not used in servers, where performance demands are significantly higher.

China's strategy is focused on import substitution rather than pushing technological boundaries. Instead of competing in the most advanced areas, such as HBM (High‑Bandwidth Memory) or server‑grade DDR5, Chinese manufacturers concentrate on replacing foreign products in mature segments and supplying cost‑sensitive markets.

Among Chinese DRAM companies, ChangXin Memory Technologies (CXMT) stands out as the most advanced and commercially viable. CXMT has reached meaningful production scale, has improved manufacturing yields, and is gradually expanding its portfolio of DRAM products. These improvements make the company increasingly attractive to consumer electronics manufacturers seeking alternative suppliers.

Fujian Jinhua (JHICC), in contrast, has made little progress. International sanctions, intellectual property disputes, and limited access to global ecosystems have largely halted its development. Although often mentioned as a DRAM player, JHICC currently lacks both technological momentum and meaningful access to customers.

The global DRAM market continues to be controlled by three major players: Samsung, SK hynix, and Micron. Their strong positions are reinforced by large manufacturing facilities located inside China, such as SK hynix's major operations in Wuxi. These facilities help secure supply for Chinese customers, but they also force local DRAM companies to compete directly with world‑leading manufacturers on their own territory.

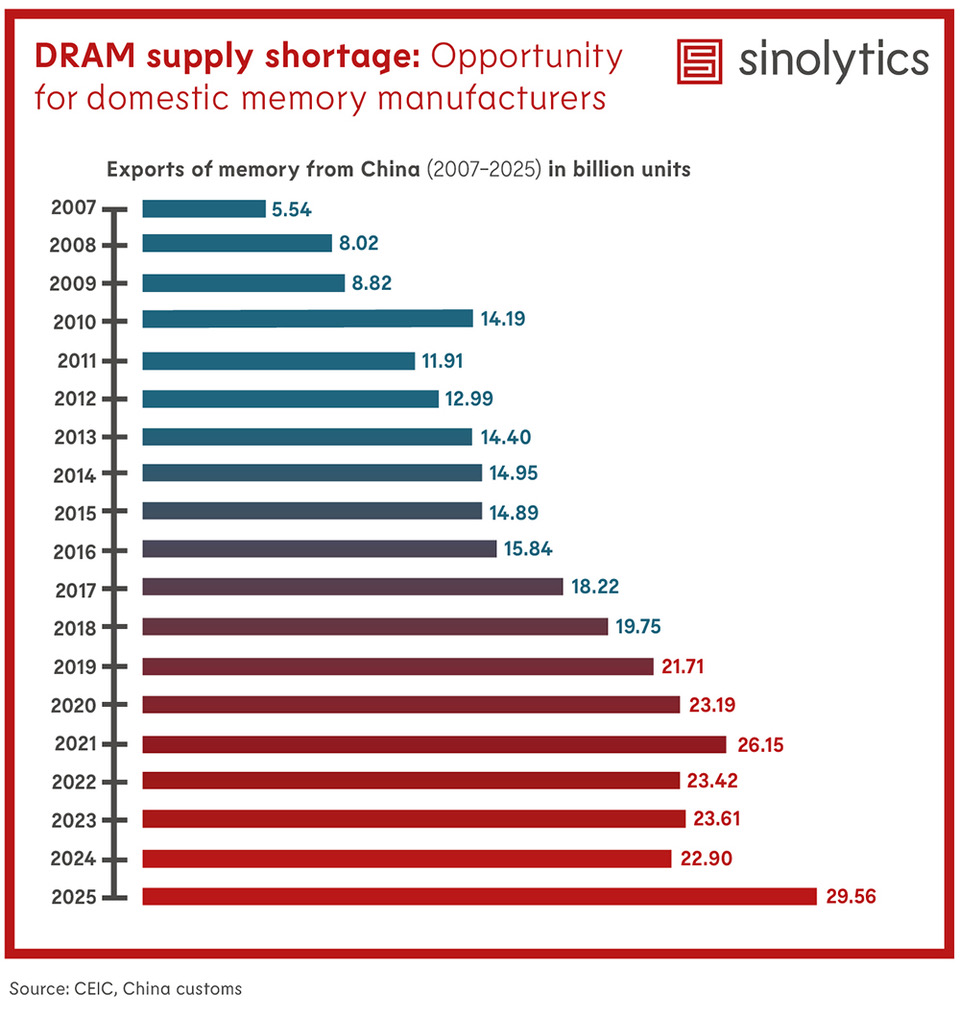

A significant portion of China's rising memory‑related exports is connected to the activities of Samsung and SK hynix in China, including packaging operations. This means that not all growth in Chinese exports reflects domestic technological advances.

As long as AI continues to absorb most of the world’s advanced DRAM capacity and production expansion remains cautious, supply for mainstream DRAM is likely to stay tight. This gives CXMT a multi‑year opportunity to increase its market share in consumer applications and memory modules. However, leadership in high‑end DRAM—especially HBM and server‑grade DDR5—is expected to remain firmly with Korean and U.S. manufacturers.