Technology

China's embodied intelligence frenzy: Capital, big tech, automakers, and policy warnings

Read more

According to data from the China Academy of Information and Communications Technology (CAICT) in December, China’s core AI industry is expected to exceed 168 billion USD (1.2 trillion CNY, 1 CNY = 0.14 USD) in 2025, representing close to 30% year-on-year growth.

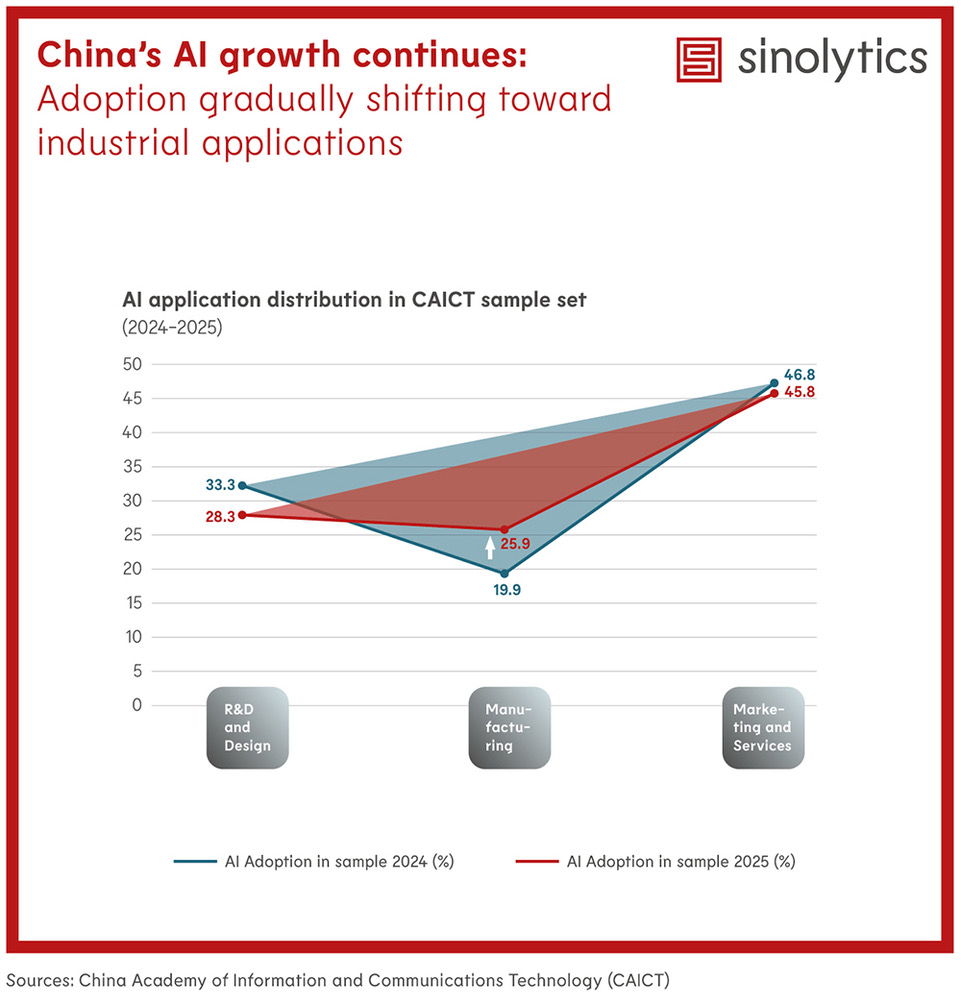

AI applications are gradually shifting from R&D and marketing functions toward production and manufacturing. CAICT data show that the share of AI applications in manufacturing increased from 19.9% in 2024 to 25.9% in 2025, signaling growing penetration into traditional industries. However, this share remains materially lower than in R&D and marketing, suggesting that deeply integrated, high-value industrial use cases have yet to reach scale.

Overall application patterns continue to display a “high at both ends, low in the middle” structure. Upstream R&D and downstream marketing show higher AI penetration, while manufacturing adoption, despite accelerating, is still focused on process optimization, efficiency improvements, and partial automation, rather than comprehensive redesign of production systems.

In manufacturing scenarios, key challenges repeatedly cited include scenario identification, data engineering, application development, and performance measurement. This indicates that the main bottleneck has shifted from access to models toward the ability to reliably deliver measurable business value, with data quality, system integration, and ROI assessment emerging as decisive factors.

Sustained policy promotion under successive “AI+” initiatives, combined with changes in data supply, is supporting wider adoption. Surveys indicate that 78% of enterprises primarily rely on industry-specific data, with industrial manufacturing, transportation, healthcare, and education as priority sectors.