China Business

China's bifurcating economy: Exports stay strong while consumption lags

Read more

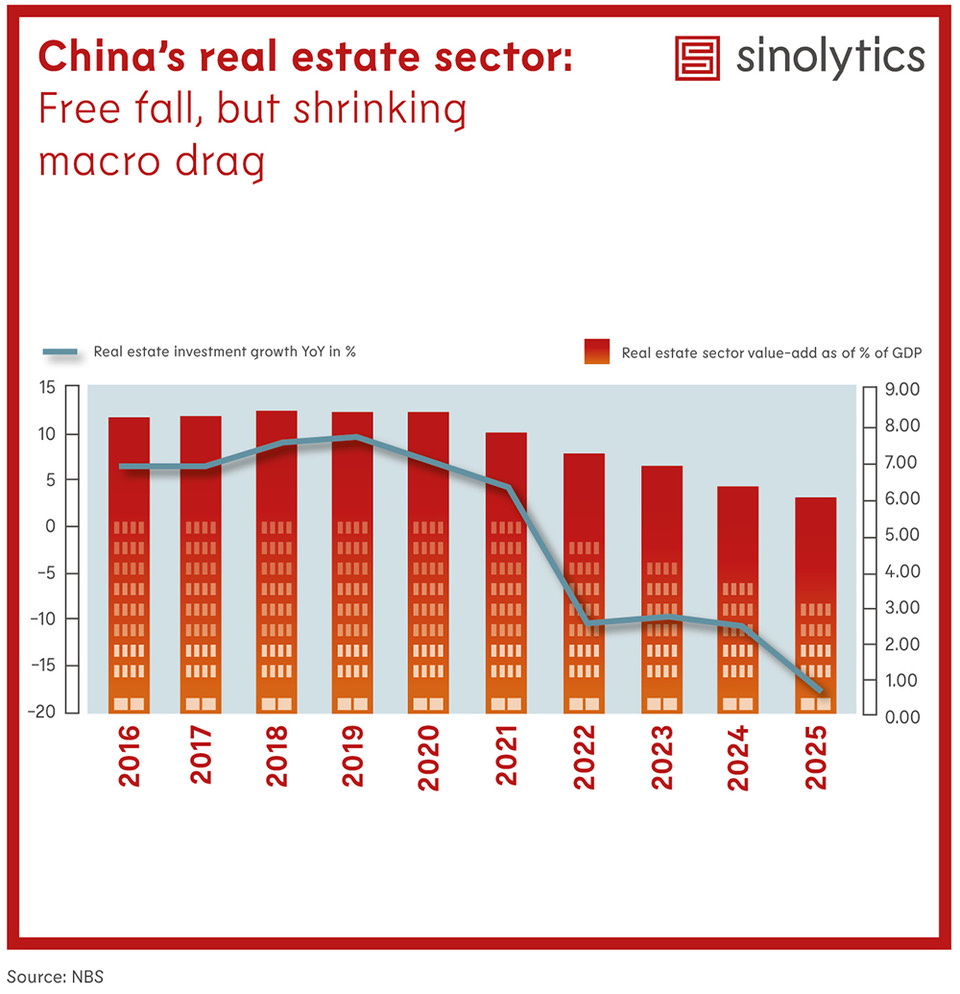

For two decades, real estate was one of China’s most powerful growth engines. That era is ending. According to the user-provided dataset, the sector’s share of GDP peaked at more than 8.28% in 2019–2020 and has been in uninterrupted decline ever since—falling to 5.92% in 2025. This marks a structural shift: even as the sector remains large, its relevance to China’s broader economic model is eroding. This trend helps explain why the sharp property contraction is not dragging headline GDP down as severely as in past cycles.

The investment collapse is stark. Real estate investment grew steadily at 6–10% annually between 2016 and 2019, moderated to +6.8% in 2020 and +4.3% in 2021, and then plunged into a multi‑year contraction: –10% (2022), –9.5% (2023), –10.6% (2024), and –17.2% in 2025. This pattern points to a prolonged investment bust without visible stabilization. Developers face tighter financing, home buyers remain cautious, and policy easing has not yet produced durable momentum.

Despite the sector’s internal deterioration, its impact on the broader economy is muting over time. The key reason: a shrinking base. With value-added declining from ~8.3% of GDP in 2019–2020 to ~6.2% in 2024 and ~5.9% in 2025, each incremental decline in real estate activity hits a smaller portion of the economy.

Beijing’s stance has shifted from trying to restart a housing boom to managing an orderly downsizing of a structurally oversized sector. Targeted support for developers, relaxation of purchase restrictions, and mortgage rate cuts aim to avoid disorderly collapse, but none signal a return to the old growth model. Policymakers appear increasingly willing to tolerate a smaller real estate economy if it stabilizes financial risks and rebalances household expectations.

The prolonged downturn affects foreign firms differently depending on sector exposure. Demand linked directly to construction—machinery, building materials, industrial systems—faces persistent headwinds. And market demand for luxury goods or services supported by household wealth are also constantly hit by the loss of property values due to price depreciation.

Meanwhile, the broader macro picture remains more resilient than sector data suggests, reducing risk of a generalized hard landing. Companies should prepare for a long, uneven adjustment rather than expect a cyclical recovery in housing-driven demand.