China Business

IP protection in China: Enforcement has improved, but gaps remain

Read more

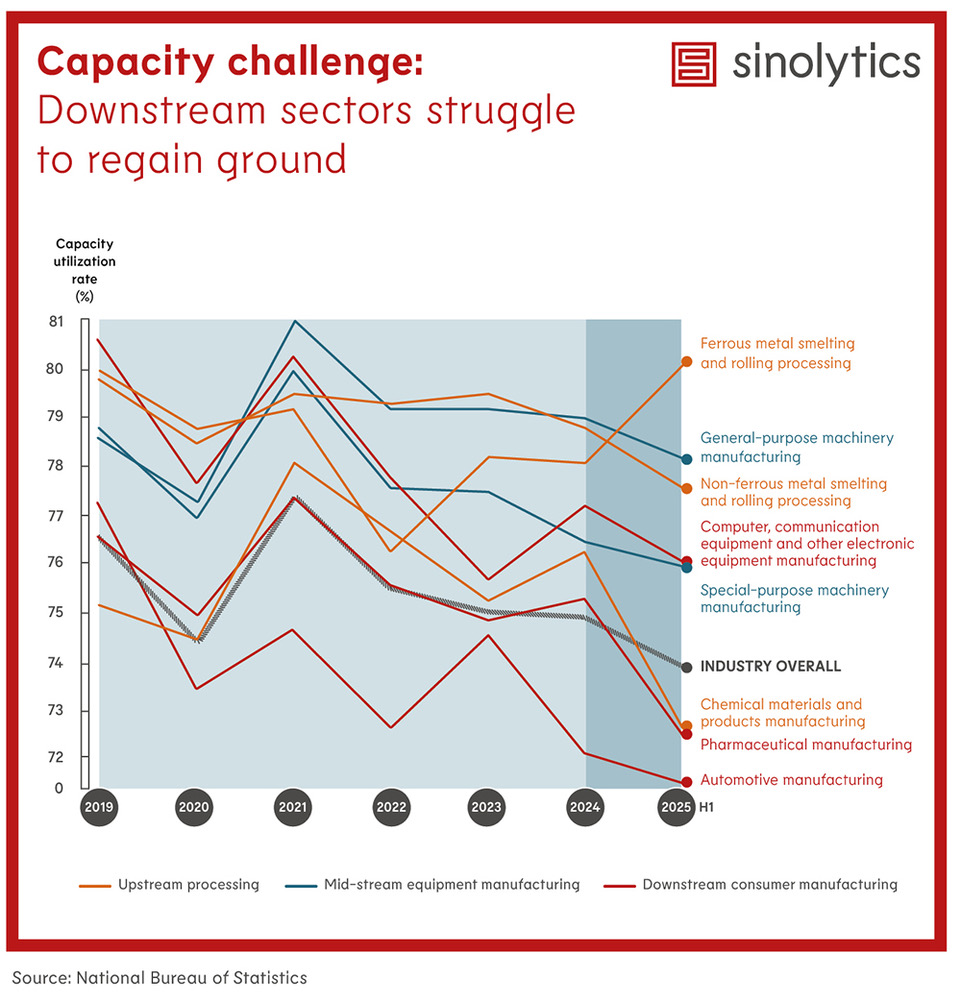

Capacity utilization rate across several key industries in China have fallen to new lows since the Covid period. While upstream processing sectors show signs of stagnation, most downstream manufacturing categories, particularly automotive, pharmaceuticals, and electronics, are operating near multi-year lows. In the automotive sector, surging NEV production has pushed the passenger car inventory to the highest level in five years as of May 2025, prompting aggressive price cuts.

Chinese regulators are escalating efforts to address what they see as “disorderly competition”, stemming from the capacity challenge. The National Development and Reform Commission (NDRC) and the Ministry of Industry and Information Technology (MIIT) have introduced measures ranging from legal restrictions on pricing practices to quality inspections and industry self-regulation pledges. The NDRC’s newly proposed amendment to the Price Law seeks to curb below-cost pricing tactics, especially targeting aspiring monopolists. While still at an early stage, these moves signal growing political will to direct the industrial economy toward quality-oriented growth.

Despite rhetorical escalation in recent high-level political meetings, tackling overcapacity will be an uphill battle, due to the deeply embedded structural imbalances in China’s economic model, misaligned local incentives, and the need to balance growth with stability. While current measures may reduce some excesses in targeted industries and curb the most disruptive pricing behaviors, without structural reforms to the underlying development and governance model, the overcapacity cycle will likely continue to repeat itself.

The “anti-involution” campaign will likely unfold as a multi-year, sector-by-sector adjustment rather than a quick fix. It may create openings for quality-focused competitors, but overcapacity and weak domestic demand will continue to shape the short-term business environment. MNCs should actively monitor policy developments from ministerial announcements to local implementation and assess business exposure to sectors targeted for state-driven consolidation.