China Business

Price wars: The cost of China’s EV dominance

Read more

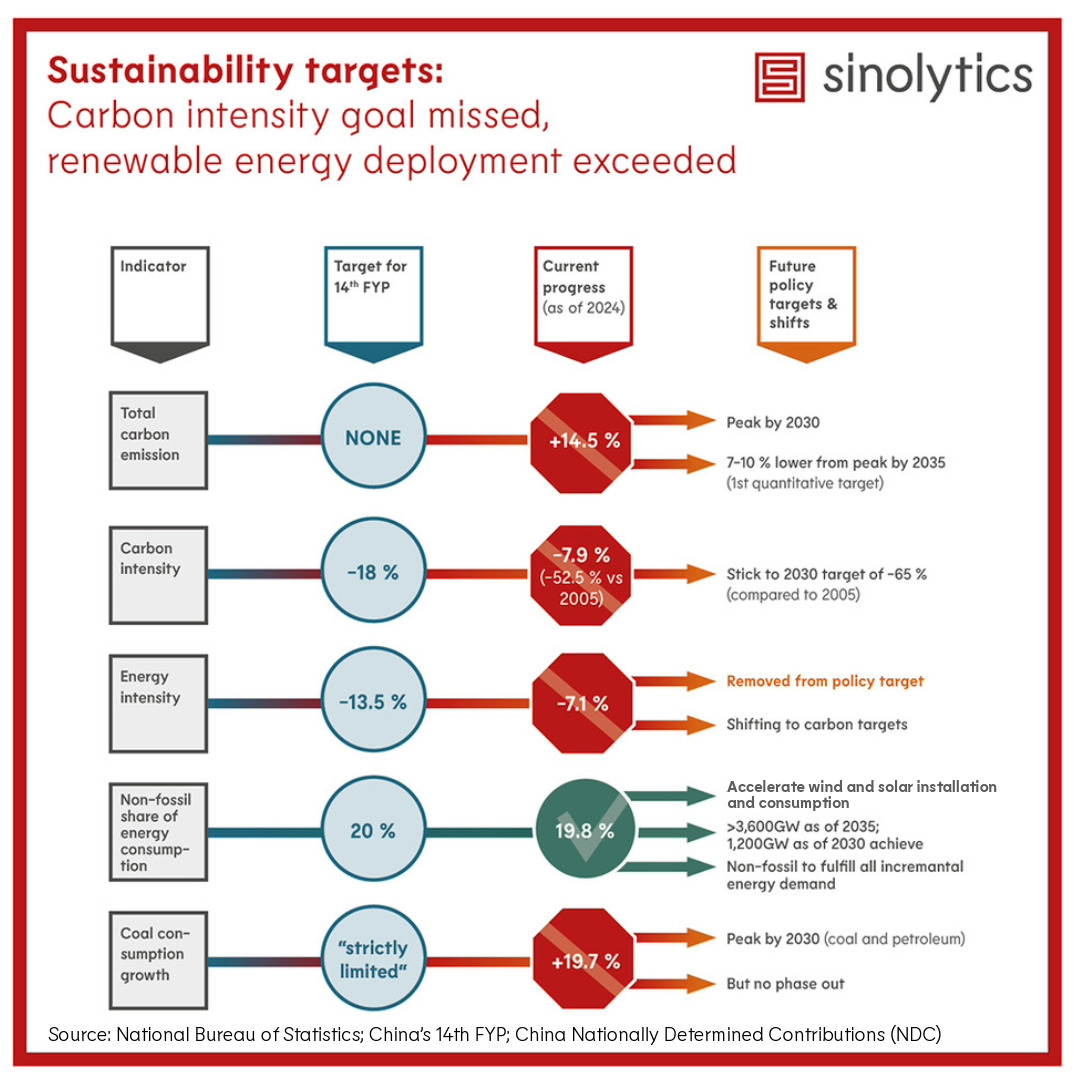

China's sustainability performance is mixed: carbon- and energy-intensity cuts are behind plan, total emissions have risen, and coal use has increased. By contrast, the non-fossil share of energy consumption is on track (around 19.8%), underpinned by strong renewable build-out. Against this backdrop, recent policy updates signal a clear pivot from managing energy intensity to emphasizing carbon-based controls, including explicit waypoints to peak national emissions by 2030 and reach 7–10% below the peak by 2035.

China is leaning on renewables and green technologies to meet energy demand and drive economic growth. The country over-achieved its 2030 wind and solar capacity goal six years early, and non-fossil power capacity now exceeds fossil capacity. Policy guidance increasingly expects non-fossil sources to meet incremental demand, aligning with the current build-out trajectory. Even from a high base, solar and wind additions are likely to remain strong, reinforcing China’s global leadership and supporting equipment exports and overseas investment.

The 15th FYP is expected to elevate hydrogen and energy storage as priority sectors. China's green hydrogen production capacity already accounted for more than half of global capacity in 2024. With continued policy support, the value chain is expected to scale from production into industrial applications. Energy storage is similarly prioritized to enhance grid resilience and energy security, with plans to nearly triple capacity by 2027. As policy support, electricity-price reform, and technological advances converge, faster installation growth, higher utilization, and improving returns are expected.

China's national Emissions Trading System is expanding from the power sector to steel, cement, and aluminum, with plans to cover all carbon-intensive sectors by 2027. The system's impact is expected to strengthen from 2027 onward through full sectoral coverage, tighter caps, and paid quota allocation. Carbon prices are therefore likely to rise over time, although a substantial gap with the EU ETS is expected to persist, creating additional landed-cost exposure under CBAM. In parallel, Green Electricity Certificates are being promoted as the main instrument to trade the environmental value of green power. Emerging green power consumption mandates for energy-intensive users, including steel and data centers, are set to boost demand and pricing, positioning GECs as a central compliance tool.

Foreign-invested enterprises should expect expanded policy incentives and funding in priority green technology sectors, particularly hydrogen and energy storage. These programs can be leveraged to identify investment and partnership opportunities across China's fast-growing green-tech value chains. As China's decarbonization toolkit matures and becomes more internationally aligned, companies can increasingly use these instruments to decarbonize local operations and strengthen compliance with international reporting requirements and CBAM.