Geopolitics

Malaysia's AI bet: Digital boom under geopolitical pressure

Read more

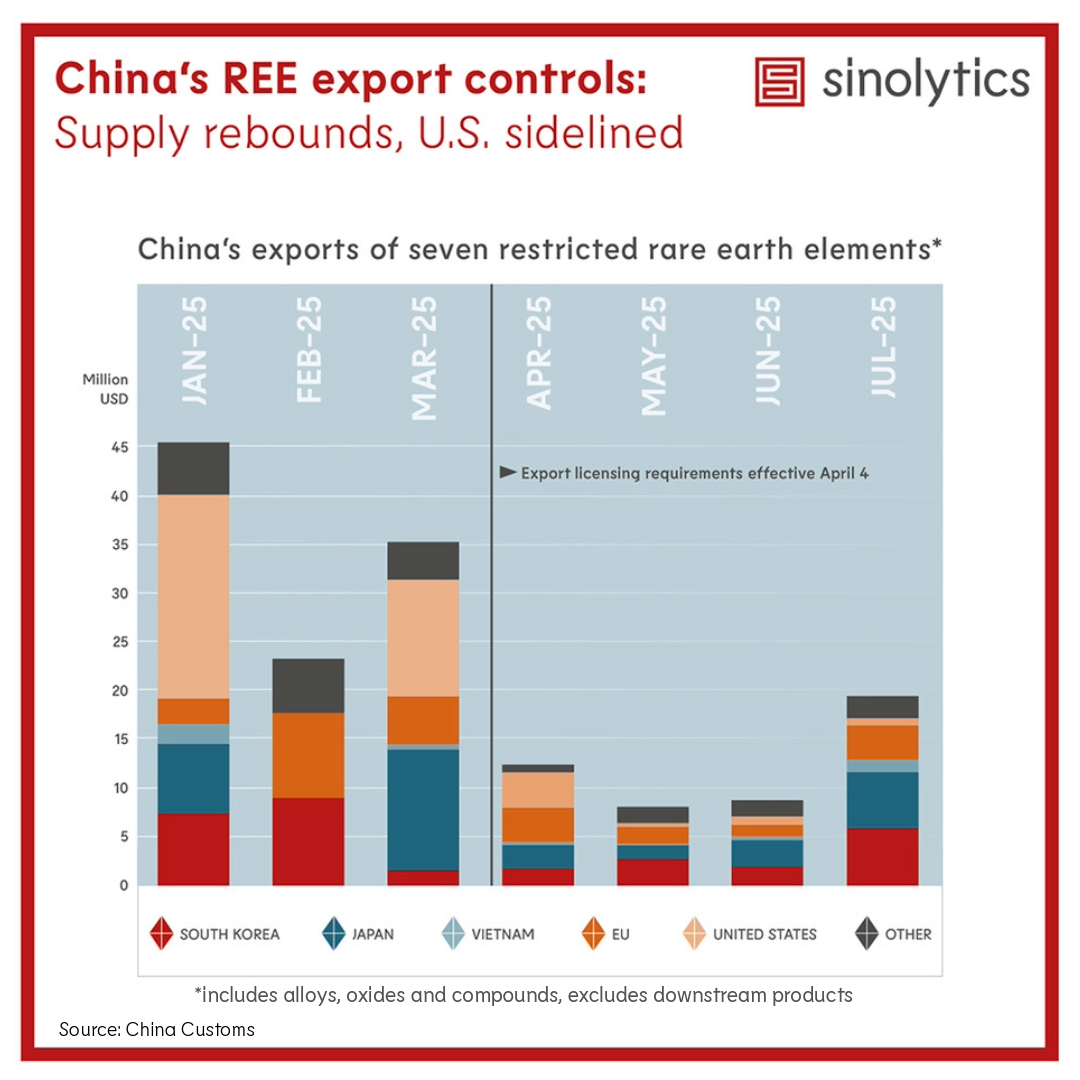

In April 2025, China introduced export

licensing requirements for seven upstream rare earth elements: scandium,

yttrium, samarium, gadolinium, terbium, dysprosium, and lutetium. Unlike

previous measures that exclusively targeted upstream raw materials and their

basic forms - oxides, alloys, and compounds, these controls also encompass

intermediate products containing REE, including permanent magnets, sputtering

targets used in semiconductor applications. The

move triggered an immediate drop in exports of these materials, particularly to

countries heavily reliant on Chinese REEs.

Shipments to the U.S. fell dramatically from over $20M in March to under $1M by

July, according to China Customs data. The sharp decline reflects both

regulatory friction and Beijing’s strategic intent to limit access to upstream

materials while maintaining leverage over global REE supply chains.

Since June, export volumes have begun to

recover, but the rebound is uneven. South Korea and Japan have seen a faster

return of supply, while U.S. volumes remain far below pre-control levels. This

divergence underscores China’s differentiated approach to trade partners and

its willingness to use REE exports as a geopolitical lever.

Interestingly, exports of downstream REE-containing products (such as permanent

magnets and specialty chemicals) are recovering more quickly, including to the

U.S. This suggests that China is selectively easing controls on intermediate

goods while keeping upstream materials tightly restricted.

The impact on U.S. manufacturers has been

significant. Industries that rely on upstream REE inputs – particularly magnet

producers – continue to face sourcing delays, cost increases, and uncertainty.

These disruptions are especially acute in sectors like defense, electric

vehicles, and clean energy, where REEs are critical for high-performance

components.

“China is loosening export controls on intermediate products like magnets under U.S. trade pressure, while keeping upstream REE materials restricted – a calculated move to sustain global dependence on China’s REE-based manufacturing ecosystem.”

This strategy allows China to maintain its dominance in REE-based manufacturing

while mitigating some international backlash by continuing to supply finished

goods.

China’s calibrated export control policy highlights its ability to weaponize supply chains without fully cutting off global markets. By restricting upstream materials while allowing downstream exports, Beijing consolidates its strategic position in the REE value chain and incentivizes foreign governments to develop alternative sources, a process that is still in its early stages.