China Policy

Early warning, not hindsight: Meet Leonhard Xu on reading geopolitical signals

Read more

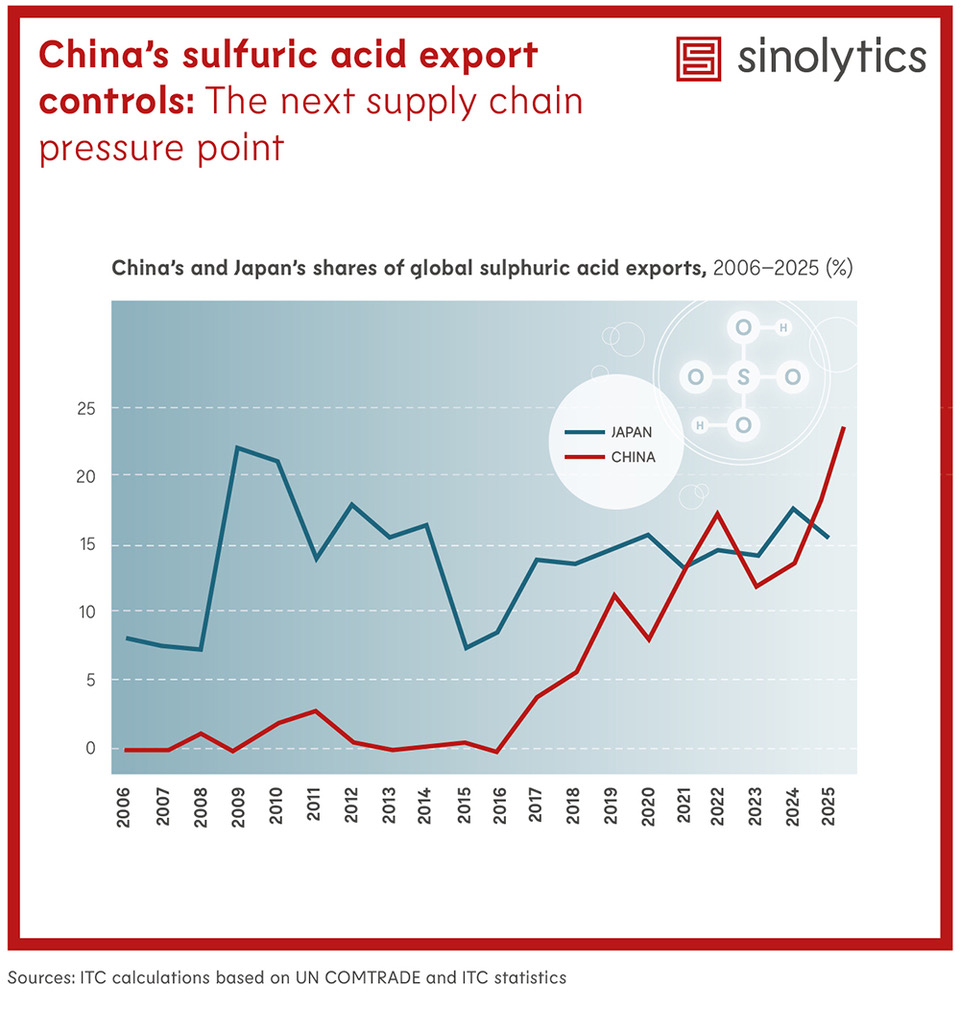

However, in response to supply disruptions in sulfur from the Middle East, China has introduced new restrictions on sulfuric acid exports. Although only around 4% of China’s sulfuric acid production is exported, authorities appear concerned about a potential surge in outbound shipments. The measures aim to safeguard domestic availability amid tightening global supply.

Sulfuric acid is a critical input in fertilizers, metal processing, petrochemicals, batteries, and semiconductor manufacturing. Any supply disruption would therefore have significant cross-industry impacts.

China’s NDRC is reportedly imposing an export quota of around 700,000t for January–April 2026, equivalent to roughly 45% of exports in the same period last year. With 384,000t already exported in January and February, only about 316,000t would remain for March and April. Compared to 590,000t exported in March–April 2025, this implies a decline of roughly 46%.

China is also reportedly planning an export halt from May, although neither the quota nor the ban has been officially confirmed. Given that China accounts for roughly one-third of global production and around 23% of exports, such a move would have significant implications for global sulfuric acid supply and prices.

Most Chinese sulfuric acid exports are directed to Chile (32%), Indonesia (15%), Morocco (12%), Saudi Arabia (12%), and India (9%). Any disruption would therefore be strongly felt—for example, around 37% of Chile’s sulfuric acid imports originate from China.

Importantly, these measures do not constitute dual-use export controls; licenses are generally granted for exports rather than tied to specific end users. However, company-level quotas are likely constraining firms’ ability to export, effectively limiting their flexibility and leverage in international markets.

These measures could have significant impacts on importing countries and the global sulfuric acid market more broadly, with particularly important implications for food security.