China Business

China's real estate sector: Free fall, but shrinking macro drag

Read more

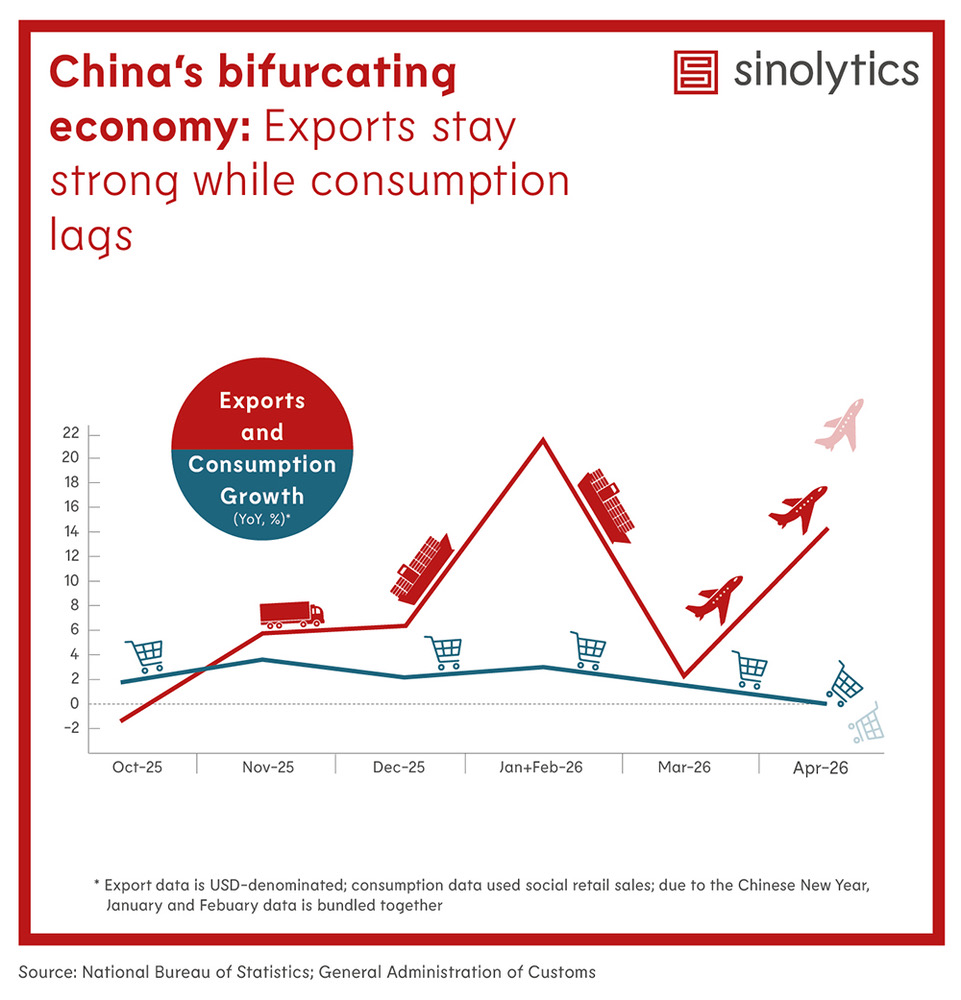

China's consumption trend stayed subdued across late 2025 to early 2026. Growth picked up to 3.1% in January and February 2026, but then weakened to 1.7% in March and just 0.2% in April. Domestic demand has not yet gained self-sustaining momentum despite the announced policy focus to promote consumption in the 15th Five-Year Plan. This is consistent with Beijing's gradual policy approach so far, rather than a large-scale stimulus response. It also explains why expectations for additional support in H2 2026 are rising.

Exports remained the bright spot. After turning positive in November 2025 and December 2025, export growth surged to 21.8% in January and February 2026, eased to 2.5% in March, and rebounded to 14.1% in April. The overall picture is one of exceptional resilience despite ongoing trade conflict pressure. Strong external demand is cushioning the economy, but this strength is not a substitute for domestic balance. It also increases the visibility of China's trade surplus and therefore its political exposure abroad.

The weaker consumption print is likely to keep pressure on policymakers. With the 15th Five-Year Plan emphasizing consumption, the current data gap underscores the upcoming challenge of translating policy intent into household spending power. A higher probability of stimulus is expected in H2 2026, especially if consumption fails to accelerate meaningfully in the next monthly releases.

China's export strength is a double-edged sword. It supports growth now, but it also increases the risk of counter-measures from the EU and the U.S., both of which remain concerned about trade imbalances. The export engine is still running well, but the more it outperforms, the more likely it is to face policy pushback abroad.