China Business

China's innovative drugs: Deepening integration into global pipelines

Read more

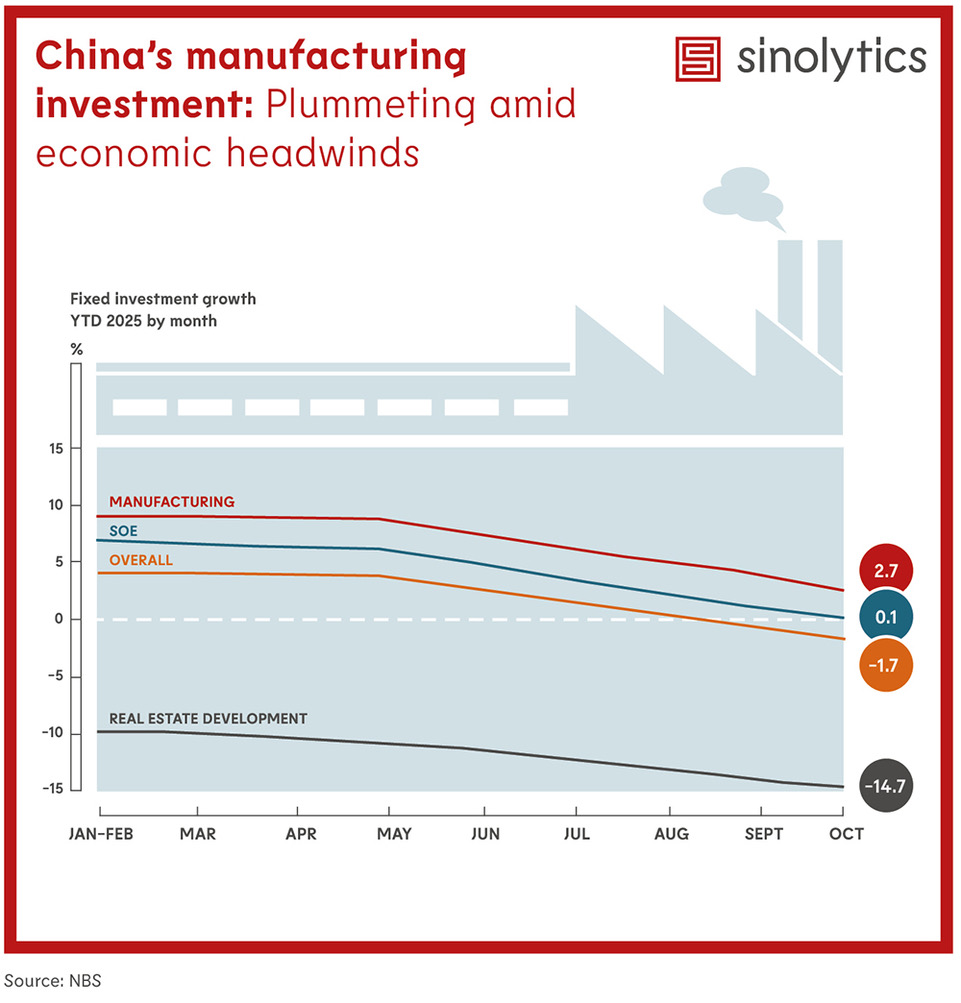

China’s fixed-asset investment growth is losing steam. Year-to-date (YTD) figures from the National Bureau of Statistics (NBS) show overall investment growth falling from +4.1% in Jan–Feb to –1.7% in October.

Manufacturing, once a bright spot, is now under pressure. Growth slowed from +9% in Jan–Feb to +2.7% in October, reflecting weakening domestic demand and global uncertainty. Analysts point to supply-chain diversification efforts and geopolitical tensions as key drivers behind the downturn.

State-owned enterprises (SOEs) maintained positive growth but decelerated sharply—from +7% early in the year to around zero by October. Meanwhile, real-estate investment remains in deep contraction, sliding further from –9.8% to –14.7%, intensifying stress across the property sector.

Beijing is expected to roll out targeted stimulus measures, with a stronger emphasis on boosting consumption rather than broad investment stimulus. Structural challenges are likely to persist, shaped by policy efforts to tackle overcapacity, weakened private-sector confidence amid declining profitability, and falling foreign direct investment.

Foreign companies in the manufacturing sector should expect continued intense competition from domestic players. The investment slowdown signals overall industry headwinds, not an easing of competitive pressure. For firms dependent on new investment—such as machinery suppliers—a slowdown in orders from downstream Chinese customers should be factored into business planning.