While some allied countries have resumed imports under license, the U.S. remains cut off. The result is a widening gap in global access to a critical material, one that plays a central role in semiconductors, optoelectronics, and defense technologies.

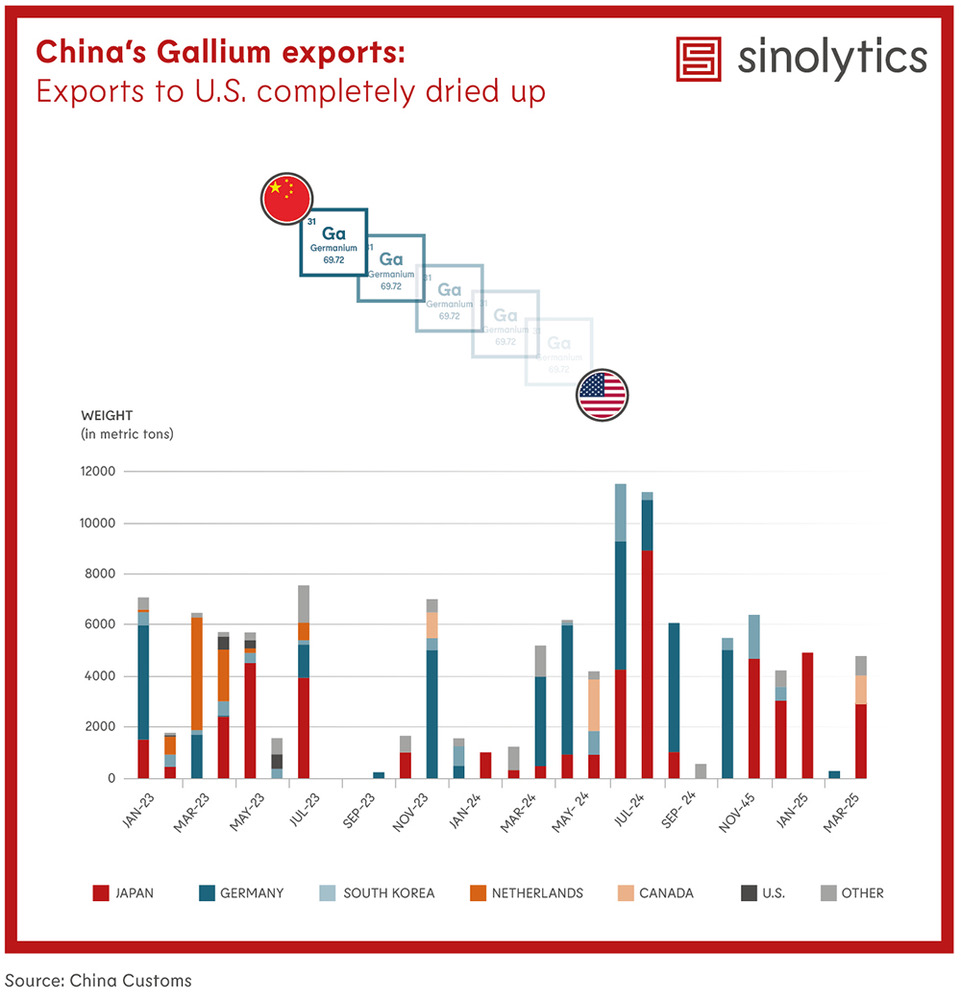

Following the introduction of export controls in August 2023, China stopped all direct gallium shipments to the United States. Although the U.S. was never a top importer, small volumes were recorded prior to the controls—these have since dropped to zero.

Other countries, including Germany, Japan, and South Korea, saw exports resume within two to three months under newly issued licenses. This selective approach highlights China’s strategic use of export permits. Shipments to Europe have been marked by fluctuations, with volumes repeatedly dropping. Overall, even these licensed flows have proven unstable: recent trade data indicates that all three countries are now increasingly facing supply disruptions as well.

In December 2024, China codified its earlier restrictions, formally embedding gallium and germanium under its export control regime. What had functioned as a de facto embargo became official policy. This move reinforced China’s ability to modulate global access to critical minerals on its terms.

In response, global producers are beginning to act. Rio Tinto announced in 2024 that it had made progress on gallium extraction at its alumina refinery in Quebec. While still early-stage, the project could eventually offer North America a domestic source of gallium.

Further afield, Eurasian Resources Group declared in June 2025 its intention to start gallium production in Kazakhstan by 2026. This marks a broader shift: efforts to reduce dependency on China are now gaining momentum—but will take time to materialize.

The developments around gallium underscore a larger trend: global supply chains tied to strategic technologies are becoming increasingly exposed to fast-moving, targeted trade restrictions. For companies in affected sectors, staying ahead means building deeper visibility into their material dependencies and preparing for continued volatility.