Geolytics

Podcast: What does tech fragmentation mean for innovation and strategy?

Read more

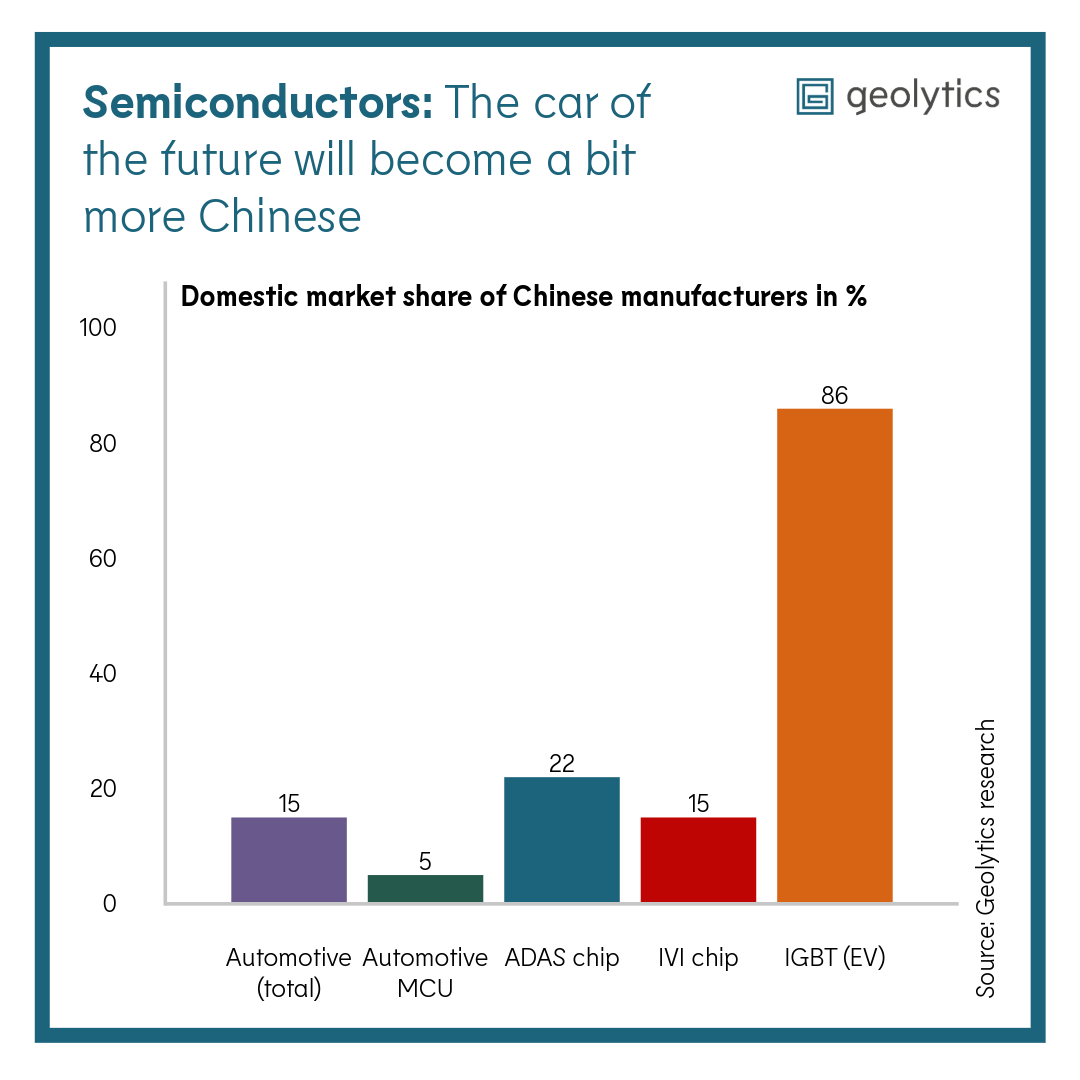

Western manufacturers such as Infineon, NXP, and STMicroelectronics still dominate many segments, but Chinese competitors are gaining ground as China’s weight in electric mobility grows. This shift is most visible in power chips (IGBTs), where Chinese producers already hold more than 80 percent of the market in China. Chinese firms are also catching up in microcontroller units (MCUs) used to manage numerous electronic vehicle functions. While their quality is improving, gaps remain in safety and longevity compared to Western suppliers.

In areas where markets and technologies are still taking shape, such as autonomous‑driving chips, Chinese firms have positioned themselves early. Horizon Robotics is one example of a company developing processors for self‑driving functions. Several Chinese automakers are also integrating chip capabilities into their own value chains: BYD manufactures its own power semiconductors, while companies like NIO and XPeng are developing chips for autonomous‑driving applications. These moves align with China’s national semiconductor strategy, which has rapidly expanded domestic manufacturing capacity. Although Western attention focuses primarily on leading‑edge AI chips, China’s growing relevance will likely be felt first in mature‑node chips widely used in the automotive sector.

Chinese semiconductor companies are expected to gain more market share, initially within China across automotive, industrial, and consumer‑electronics applications. But global ambitions are increasingly visible, particularly in memory chips, where demand from data centers has driven prices sharply upward. At the same time, Chinese firms benefit from strong domestic support, reinforced in China’s new 15th Five‑Year Plan, which again emphasizes technological self‑reliance.

Outside China, however, they face significant hurdles: cybersecurity concerns, regulatory scrutiny, and fears of a market influx of mature‑node Chinese chips. For Europe, China’s semiconductor trajectory underscores the importance of innovation‑friendly environments and strong technology clusters, supported by well‑designed state policies, to stay competitive in automotive semiconductors.

Originally published on F.A.Z. in German.