Geolytics

Why India is not an alternative to China

Read more

A central catalyst is the U.S. BIOSECURE Act, which—after two years of debate—prohibits federal agencies from contracting certain biotech firms. Existing contracts may continue until 2032, but multinational companies have already begun reassessing every node of their R&D, manufacturing, and supplier networks.

Asian governments are moving rapidly to reduce external dependencies and strengthen domestic capabilities. Japan uses its Economic Security Promotion Act to classify pharmaceuticals as “specified essential goods,” enabling subsidies for domestic production. India targets reduced reliance on foreign intermediates and active ingredients through targeted support programs. South Korea’s 2025 Synthetic Biology Promotion Act aims to expand biotech infrastructure and R&D capacity. Despite differing strategies, the political logic is consistent: pharmaceutical resilience is becoming a national security priority across the region.

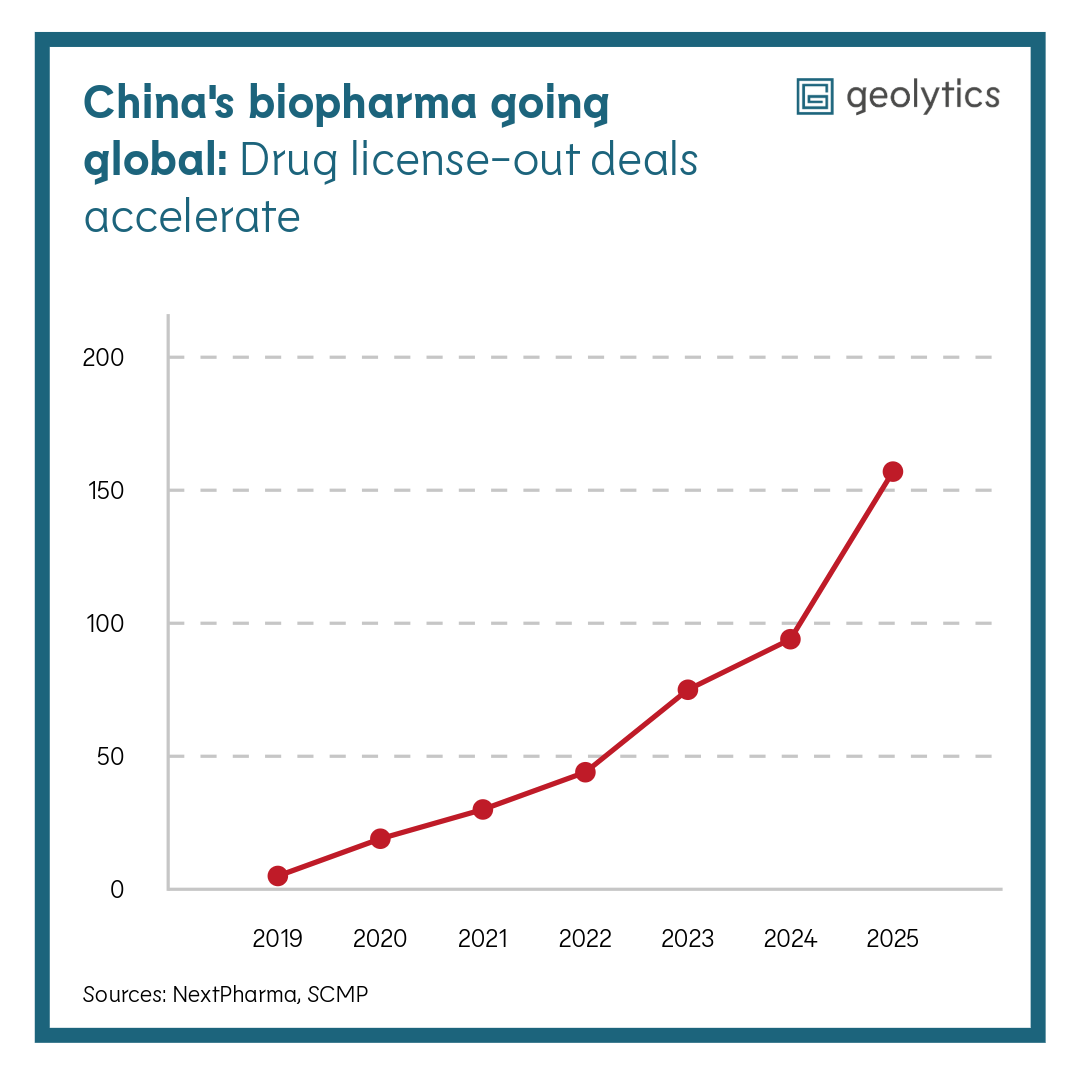

At the same time, Chinese pharmaceutical companies continue their aggressive global expansion — moving beyond generics into innovative drug development. China restricts the outflow of health and clinical data since 2025 while encouraging outward licensing. The effects are significant: 157 licensing deals with foreign companies last year valued at USD 136 billion, up from 94 deals worth USD 52 billion the year before. Average deal value has tripled since 2022. However, these partnerships also introduce geopolitical complications. Outward expansion contrasts sharply with Beijing’s focus on inward data control and domestic autonomy, creating structural asymmetry for multinational partners.

To navigate rising restrictions, many multinational companies adopt a dual operational structure: localizing data and production inside China while building parallel networks across India, Singapore, Ireland, and the United States. Strategic partnerships allow firms to overcome regulatory barriers and preserve global reach. Yet deeper collaboration with Chinese biotech poses long‑term risks. Access to production, data, and upstream supply chains forms part of China's geo‑economic toolkit. Without clear guidance from governments on where cooperation is acceptable, companies risk drifting into structural dependencies similar to those already visible in the generics market.

Originally published on F.A.Z.