Geolytics

Battery supply chains under pressure: Dr. Jost Wübbeke explains

Read more

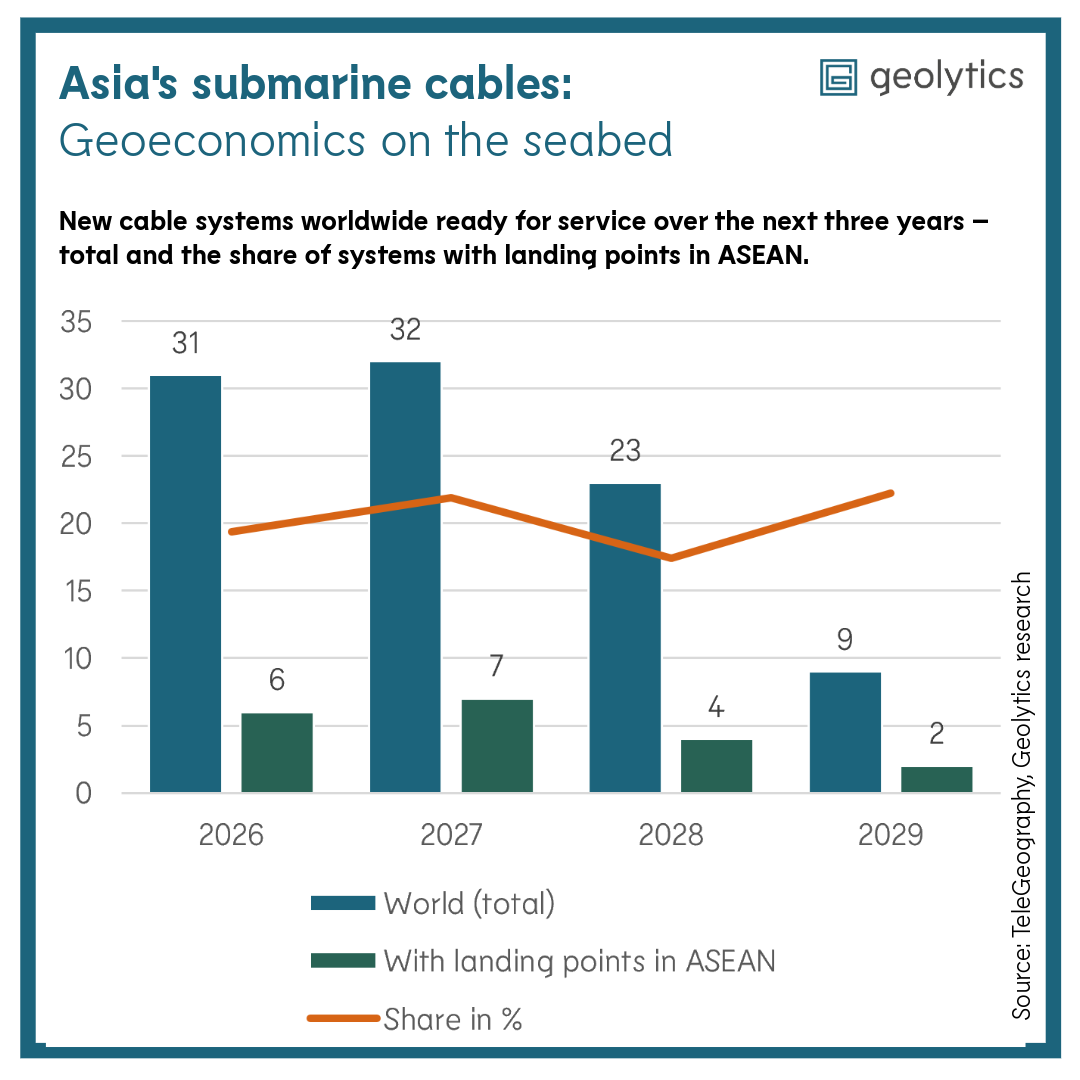

Where cities were once the primary points being connected, today it is the data centers. Submarine cables are becoming a strategic lever for emerging digital economies: their presence, capacity, and resilience ultimately shape investment decisions. And the buildout is happening fast: roughly one fifth of all systems set to be ready for service over the next three years have landing points in ASEAN; together these systems add up to around 118,000 kilometers.

The field of players is small: Alcatel (France), SubCom (United States), NEC (Japan), and HMN Tech (China) have dominated the market so far. But hyperscalers are increasingly entering the field as well: Google, Meta, Microsoft, and Amazon. Google and Meta illustrate this vividly, for instance with the intra-Asian cable system Apricot (completion 2025), Meta's Candle (planned completion 2028, so far the highest-capacity system in the Asia-Pacific region), and the transpacific system Echo (completion 2025). That puts them in a powerful position: whoever builds and finances cables is also directly involved in creating corridors, landing points, and data hubs. Put plainly, these investments directly influence the trade and investment geography of Southeast Asia's digital economy.

Beijing has embedded submarine cables in its "Digital Silk Road" and is promoting the expansion of fiber optics. In 2024, however, "only" around eleven percent of submarine cables were in Chinese hands. Governments in Washington, Tokyo, and Canberra fear dependence on Chinese infrastructure. These security concerns also show up in practice: under U.S. pressure, the SEA-ME-WE 6 cable (running from France, through the Middle East, to Southeast Asia) went to the more expensive provider SubCom, and against the Chinese competitor HMN Tech. The Apricot and Echo projects were routed around the South China Sea; the United States, India, Japan, and Australia jointly pledged more than 140 million dollars for Pacific cables. Western consortia and the hyperscalers are increasingly avoiding Chinese territory; in return, Beijing is building its own China-centered network through its state-owned enterprises, such as SEA-H2X or the planned EMA cable to France.

Driven by governments, network operators, and hyperscalers, major efforts are underway to bypass vulnerable routes and create additional redundancies. New submarine cables are expensive, yet looming outage costs and sanction risks turn resilience itself into an economic factor. This matters in particular for the islands and archipelagos of Southeast Asia. They depend on just a few corridors for international connectivity; for the platform economy and data-intensive services, "cable resilience" is becoming a precondition for lasting growth.

In Southeast Asia, submarine cables determine the cost, speed, and resilience of data flows, and with them, investment in AI, cloud, and data centers. The competition is shifting from the question of who is connected to the question of how and by whom. The hyperscalers bring the capital and the cables, the states bring the permits, and with them the final say. Where the two meet, it is decided whose logic shapes the new map of digital value creation. On that map, connectivity is as contested as energy or rare raw materials.

Originally published on F.A.Z. in German.

The header image was generated using AI and is provided for illustration purposes only.