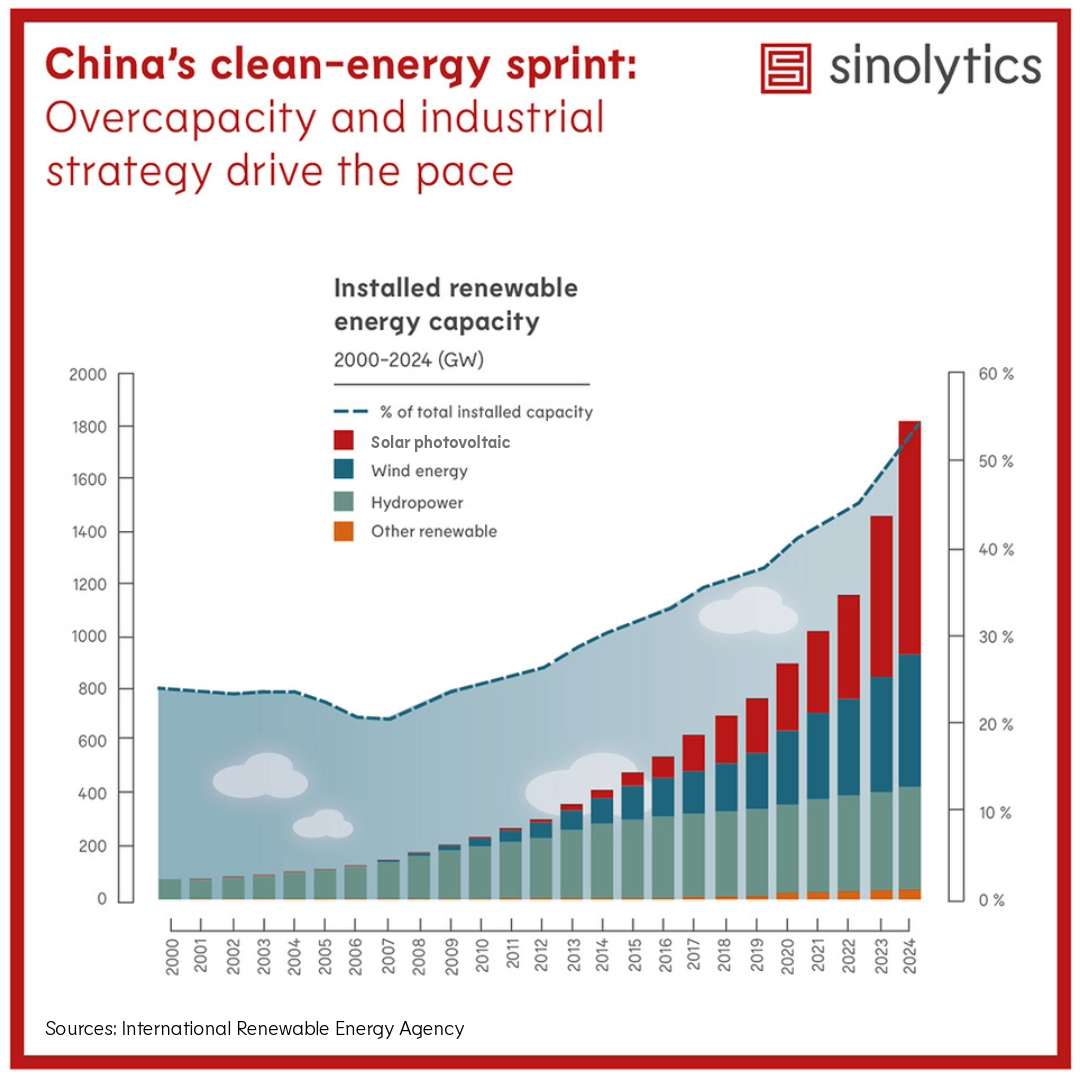

China more than doubled its installed renewable capacity from 896 GW to 1,826 GW between 2020 and 2024. This allowed the country to hit its 1,200‑GW wind‑and‑solar target in late 2024—six years ahead of plan. If installations continue at this pace, the 2035 goal of 3,600 GW could be reached as early as 2030.

Renewables now account for more than half of China's total installed power capacity. But generation still lags behind: renewable sources provided only about 40% of China’s electricity in 2025. The gap is driven by lower capacity factors of wind and solar, which cannot generate power continuously.

China produces more than 80% of the world's solar panels, wind turbines, and batteries, leading to massive industrial overcapacity that must be absorbed domestically. Accelerated renewable installation also supports broader goals: stimulating growth in a slowing economy and strengthening energy security by reducing fossil‑fuel imports.

China's rapid clean‑energy expansion is reshaping global competition in photovoltaics, batteries, and wind technology. Companies operating in or with China must anticipate intensified price competition, shifting supply‑chain dependencies, and more aggressive Chinese industrial policy in overseas markets. The combination of overcapacity and strategic state support is likely to continue exerting downward pressure on global clean‑tech prices, creating opportunities for procurement but risks for margins and existing partnerships.

Companies currently ask us questions such as:

Sinolytics helps executives answer these questions through deep‑dive market analysis, technology and supply‑chain mapping, competitive intelligence, and scenario modelling.

China's accelerated clean‑energy expansion is already reshaping global technology competition, pricing dynamics, and supply‑chain dependencies. If you want to understand how these developments intersect with your company’s strategic exposure, our experts can help you.